OUSD Is the Anti-Tether: 140 Companies Just Built a Stablecoin Designed to Give Its Profits Away

Tether cleared more than $10 billion in net profit last year by holding Treasury bills and keeping the interest. That is the entire business. No risk worth the name, just the float on roughly $186 billion in reserves, compounding quietly while holders earn zero.

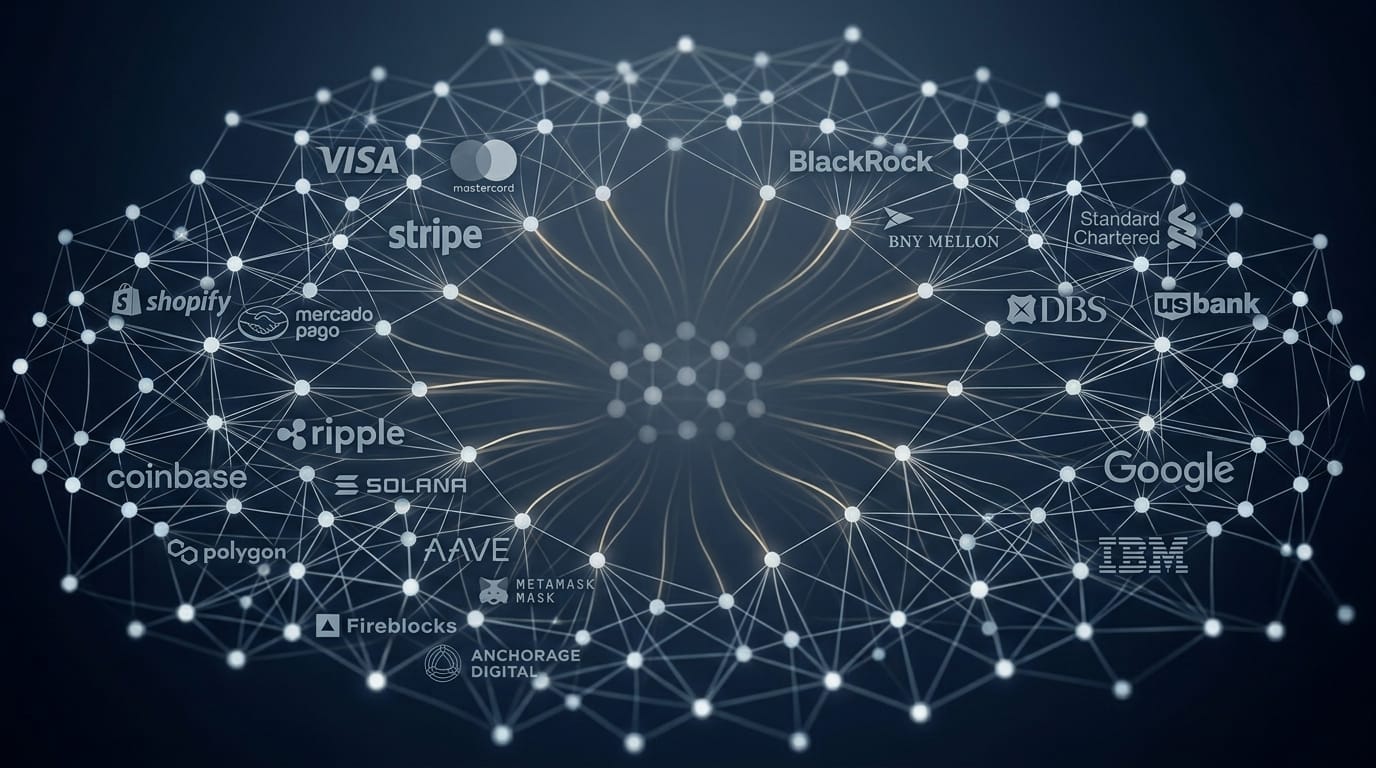

This morning, 140 of the largest names in finance and technology announced a stablecoin built to give that money away.

It is called Open USD, or OUSD, and the backer list is the story. Visa, Mastercard and American Express, networks that compete for the same swipe, signed the same document. So did Stripe, BlackRock, Coinbase, Google, BNY Mellon, Ripple and Standard Chartered. The issuer is a new, deliberately independent company called Open Standard, run by Bridge co-founder Zach Abrams, and the pitch is that OUSD belongs to no one. Mint and redeem cost nothing at any volume. Most of the reserve income flows back to the companies moving the coin, minus a small management fee. Governance sits with a board of partners rather than a single founder with a printing press.

Strip away the logos and you are looking at an attack on the most profitable model crypto ever produced.

The float was always the whole game

Here is the thing almost nobody outside the industry understood about stablecoins until recently: the holder is the product. You hand over a dollar, you get a token worth a dollar, and the issuer takes your actual dollar and buys government debt with it. At 4 to 5 percent, on hundreds of billions, the spread becomes a fortune. Tether's haul rivals Goldman Sachs, with a fraction of the staff.

Circle plays the same game with a twist — it shares roughly half its reserve income with Coinbase, which is why Coinbase pays yield on USDC while Circle's own margin looks thin. The float still does the work. It just gets split one way instead of hoarded.

OUSD's founders looked at that arrangement and asked the uncomfortable question. If the reserve income is the prize, why should the issuer keep it? Why not route it to the hundreds of businesses actually generating the volume?

That is the whole design. And it only makes sense if you remember what happened the last time someone tried this.

This is Libra, rebuilt to survive

In 2019, Facebook tried to launch a global stablecoin and got dismembered by regulators who saw one company reaching for monetary power. The project died. Its chief economist, Christian Catalini, now argues OUSD revives that vision — an open protocol for digital dollars — with the one change that matters. No single owner.

Read the structure as a regulatory strategy, because that is what it is. Libra was a target because Mark Zuckerberg would have controlled it. OUSD is harder to attack precisely because 140 rivals control it together, and a consortium of competitors makes a clumsy villain in a Senate hearing. Distributed ownership is not a feel-good detail here. It is the moat.

The timing helps. The GENIUS Act, signed in July 2025, finally gave dollar stablecoins a federal rulebook — 1:1 reserves and monthly attestations. The rails are legal now in a way they were not when Libra was buried. A neutral standard has a place to stand.

The yield doesn't go to you. It goes to them.

Now the part that should make you pause.

The GENIUS Act bans issuers from paying interest or yield to the people who hold the coin. OUSD obeys that. Holders still get nothing. What partners receive is something the statute left murkier — reserve income shared with the businesses that distribute the token, characterized as a commercial arrangement rather than interest to a holder.

That distinction is the single most contested question in stablecoin policy right now. More than 40 banking associations, led by the American Bankers Association, are lobbying Congress to slam this exact door shut, warning that yield routed through affiliates and distributors will drain deposits out of the banks that fund Main Street lending. Regulators have already floated rules to extend the prohibition to affiliates and third parties.

So OUSD's headline feature — share the reserve revenue with the network — sits squarely on top of the loophole the most powerful lobby in American banking is spending 2026 trying to close. Bold. Maybe too bold. The design is elegant, and the regulatory ground underneath it is actively shifting.

Now argue the other side

Here is the strongest case against OUSD, and it has nothing to do with regulators.

Consortiums are where ambition goes to die. You have assembled Visa and Mastercard and Amex — firms that have spent decades and small fortunes suing each other — and told them to agree on governance, reserve policy, chain support and revenue splits, in a room, repeatedly, forever. The reason Tether wins is embarrassingly simple: one person decides, and decides fast. Paolo Ardoino does not convene a board of 140 competitors to approve a Treasury allocation.

Even Catalini, making the bull case, concedes the hard part comes after the press release — getting fierce rivals to actually converge on shared standards rather than quietly defect. Everyone smiles at the announcement. Then the working groups meet. A standard that 140 companies co-own is a standard 140 companies can each slow down.

I think the structure is genuinely clever, and I would still bet the execution is brutal.

The announcement was the easy part

Which surfaces the question OUSD has to answer next, and it is not a marketing question. It is a plumbing one. When 140 competitors agree to share revenue and govern collectively, what enforces the agreement once the enthusiasm fades and incentives drift?

In crypto, that answer increasingly lives on-chain rather than in a contract nobody reads. Locking allocations and enforcing vesting schedules — making commitments programmatic so no party can quietly walk them back — is the unglamorous layer every multi-party token arrangement eventually needs. Team Finance handles exactly that friction for projects: tokens locked and schedules enforced, the rules made mechanical instead of trust-based. A consortium of rivals is precisely the situation where mechanical beats trust.

Because the test for OUSD was never whether 140 logos could share a stage for one morning in June. It was whether they can share an economy for a decade. Tether built a $10 billion machine on the premise that the holder will never demand the float back. OUSD is a bet that the float was never the point — that in a market where the yield gets shared rather than hoarded, the winner is the neutral standard everyone can build on.

One of those bets is printing money today. The other one hasn't issued a single coin.

So which model looks fragile to you now — the one earning ten billion a year, or the one trying to give it away?